As the banking process outsourcing market is projected to grow at a robust 9.1% CAGR by 2030, medium- and large-sized companies are increasingly outsourcing their banking and financial services to save time, optimize resources, and accelerate growth.

This steady expansion is driven by the rising demand for dependable, cost-effective solutions, the adoption of advanced technologies, and the growth of the BPO industry in emerging economies.

For banking, financial services, and insurance (BFSI) organizations, outsourcing has become an important piece of their strategies, improving operational efficiency, regulatory compliance, and fast scalability.

How can business process outsourcing help your organization improve client interactions and streamline back office operations? In this article, we’ll explore how BPO benefits BFSI companies, drives growth, and more.

Key Takeaways

- BPO drives efficiency: Outsourcing non-core banking and financial processes allows institutions to reduce operational overhead, streamline workflows, and focus internal resources on strategic priorities.

- Compliance and risk management: Banking BPO ensures adherence to regulations like GLBA, AML/KYC, and PCI DSS, helping mitigate compliance risks and maintain data security.

- Scalability and agility: Institutions can quickly scale operations during peak periods, expand into new markets, or launch products faster without building large in-house teams.

- Access to specialized talent and technology: BPO providers deliver expertise across the BFSI sector and integrate tools like AI, RPA, and cloud platforms to improve efficiency, accuracy, and customer experience.

- Partner with Sourcefit for results: Sourcefit offers flexible, scalable, and compliant outsourcing solutions across front, middle, and back office, helping organizations reduce costs, improve operational efficiency, and achieve growth objectives.

What is business process outsourcing (BPO)?

| Banking and financial services outsourcing involves delegating specific business tasks to a third-party provider to save time and resources. |

BFSI organizations outsource non-core tasks while focusing on strategic responsibilities that drive growth, enhance customer experience, and ensure compliance with evolving regulations.

Common business operations outsourcing tasks include accounting, payroll, human resources, customer support, IT services, and procurement. These are essential tasks that keep the business running smoothly but fall outside the company’s core value proposition.

With the help of outsourcing, companies can scale efficiently without the overhead of hiring and onboarding new staff or spending resources necessary to optimize other core operations.

BPO vs. Shared services vs. Staff augmentation

Business and financial services outsourcing shouldn’t be confused with shared services and staff augmentation.

BPO involves subcontracting an external provider to manage certain tasks, such as accounting or customer service. In this model, the BPO partner takes full responsibility for executing delegated tasks and does not require the involvement of the internal team.

Shared services, on the other hand, are a high-investment approach that creates centralized departments like HR, IT, or Finance. Each serves multiple divisions and maintains full internal control.

Staff augmentation is the combination of the two models. A company hires a talent only for a certain period to fill skill gaps or manage seasonal workload.

Why BFSI companies prefer business process outsourcing

BPO has proven efficient across industries, including highly regulated ones such as healthcare, insurance, and finance. This is because every niche has administrative responsibilities that can be offloaded to outsourcing providers at a lower cost than hiring a full-time talent.

Each company handles back office tasks daily that are critical to keeping the business running smoothly, but are not considered core responsibilities. When workloads spike or the company scales, it may not have the resources to hire full-time staff, so outsourcing becomes an efficient way to manage these essential yet non-core tasks.

Types of business process outsourcing

Business and financial process outsourcing can be divided into three key categories:

Onshore BPO

Onshore BPO refers to outsourcing to a provider that is located in the same country as your business. It is often used in financial services due to the compliance concerns, sensitive customer data handling, and specialized accounting processes.

Pros:

- Easier communication

- Full regulatory alignment

- Faster response times

Cons:

- Higher cost compared to offshore or nearshore outsourcing options

Nearshore BPO

Nearshore BPO refers to partnering with a provider that is located in nearby countries. Such providers are often located in the same time region or time zone. U.S.-based companies outsource back office support to Latin American countries because of geographic proximity and overlapping time zones.

Pros:

- Regional proximity

- Same or similar time zone

Offshore BPO

Offshore BPO involves outsourcing to distant countries. This type often comes with lower labor costs and access to a larger talent pool. The Philippines is one of the most popular choices for BFSI outsourcing due to its skilled workforce, English proficiency, and affordable cost.

Pros:

- Significant cost savings

- Scalability

- Access to specialized skills not readily available locally

BPO market highlights (2025–2026)

The global BFSI BPO services market was valued at $124.86 billion in 2024 and is projected to reach $230.08 billion by 2033. The growth is driven by fintech expansion, AI automation, and regulatory demands.

Automation

The adoption of automation technologies is rapidly reshaping the landscape of Banking BPO and financial services.

Robotic Process Automation (RPA), Artificial Intelligence (AI), and machine learning are being integrated into various processes to streamline operations, enhance efficiency, and reduce human errors.

AI and RPA adoption in Banking BPO has accelerated, enabling over 70% cost savings in finance back office functions like invoice processing, KYC verification, and claims handling.

Cloud-based products

The migration to cloud-based solutions is revolutionizing how banking and financial services are delivered and managed. Cloud technology provides secure and scalable platforms that facilitate seamless access to data, applications, and services from anywhere, at any time.

This shift allows financial institutions to respond more swiftly to changing market demands, provide personalized services, and optimize their IT infrastructure, leading to enhanced customer experiences and increased operational agility.

Online banking

The rise of online banking is reshaping how consumers interact with their financial institutions. With the convenience of 24/7 access, customers can conduct a wide range of banking activities through web and mobile applications.

Online banking empowers customers to manage accounts, make transactions, pay bills, and even apply for financial products from the comfort of their homes.

Financial institutions are investing in user-friendly interfaces, robust security measures, and personalized digital experiences to meet the evolving needs of tech-savvy consumers and attract a broader customer base.

Data analytics and insights

The increasing reliance on data analytics and insights is transforming how financial institutions make strategic decisions and engage with customers.

Advanced data analytics tools and technologies enable banks to extract valuable insights from vast amounts of data, enabling them to offer personalized products, anticipate customer needs, identify fraud, and assess risks more accurately.

Cybersecurity and privacy

With the growing digitalization of financial services, cybersecurity and data privacy have become paramount concerns.

Rising AI-driven ransomware and supply chain threats demand proactive measures like quantum-resistant encryption, third-party oversight, and real-time threat detection via AI/ML in BPO.

Strict regulations like GLBA and PCI DSS drive outsourcing for 24/7 monitoring and biometric authentication to protect digital banking data. Incidents like data breaches necessitate coordinated intelligence sharing and robust compliance frameworks.

Mobile banking and digital payments

Mobile banking and digital payment solutions are gaining significant momentum as consumers increasingly prefer convenient, contactless, and secure methods of conducting financial transactions.

Financial service providers are investing in user-friendly mobile apps, digital wallets, and innovative payment technologies to cater to the evolving preferences of tech-savvy customers.

BPO streamlines payment processing, fraud detection, and wallet integration for frictionless transactions.

Personalization and customer experience

Delivering personalized experiences is becoming a key differentiator in the financial services industry.

Banks are leveraging customer data and AI-powered algorithms to offer tailored financial solutions, personalized product recommendations, and customized communication to enhance overall customer satisfaction and loyalty.

BPOs enable autonomous operations like onboarding and treasury with personalized services. 53% of consumers share more data for better insights if experiences improve.

Regulatory compliance

Stringent regulatory requirements continue to impact the banking and financial services sector. To stay compliant with changing regulations and avoid penalties, financial institutions are investing in specialized compliance teams, technologies, and BPO services to ensure adherence to industry standards.

2026 priorities include ESG disclosures, sustainability standards, and oversight of rating providers. Automated tools ensure adherence in cross-border operations and fintech partnerships.

ESG (Environmental, Social, and Governance) focus

A growing trend in the financial services industry is the increasing emphasis on Environmental, Social, and Governance (ESG) factors.

Investors and customers are looking for financial institutions that prioritize sustainability, social responsibility, and ethical practices, leading to a shift in investment strategies and the integration of ESG considerations in financial decision-making.

As these trends continue to evolve, the Banking BPO and financial services industry will witness significant transformations, leading to greater efficiency, improved customer experiences, and a more competitive market landscape.

Embracing these trends will be crucial for organizations seeking to stay ahead and thrive in the ever-changing financial services sector.

What is banking process outsourcing?

| Banking BPO is a subset of BPO that specifically focuses on outsourcing processes related to banking and financial services. |

Business Process Outsourcing is a broad term for services that can include HR, IT support, or customer service. In contrast, banking BPO refers to services like loan processing, mortgage servicing, back office accounting, and others.

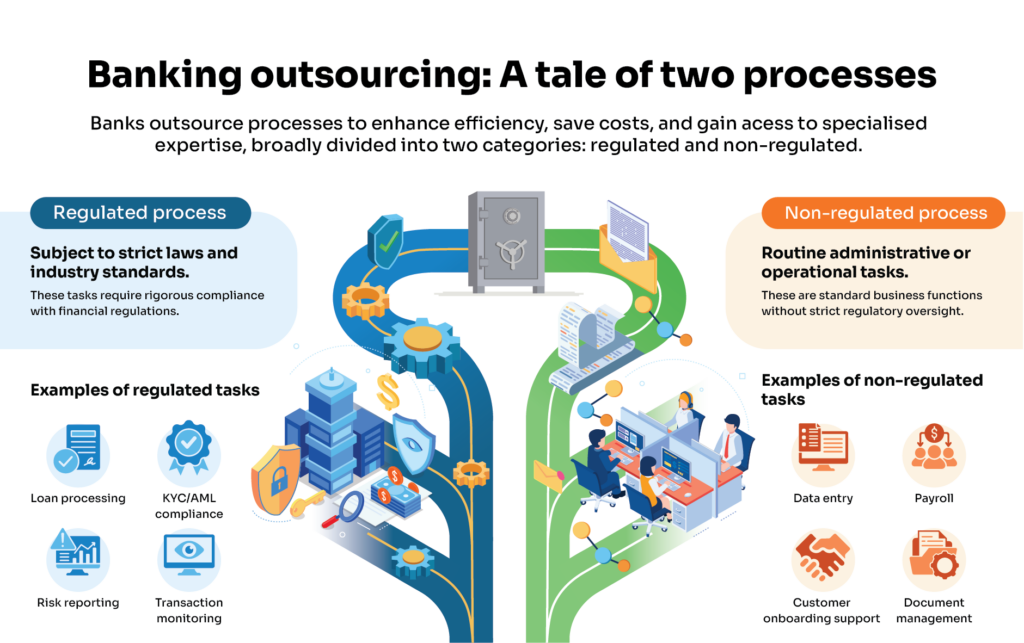

Banks outsource both regulated and non-regulated processes to optimize their efficiency while saving costs. Outsourcing helps them get access to specialized expertise that will maintain compliance in the financial environment.

Bank BPO is a strategic decision to outsource services across front, middle, and back office to achieve cost efficiency and regulatory compliance while focusing on the core business:

- Front office: Customer-facing functions like call centers, relationship management, and support services.

- Middle office: Risk management, compliance monitoring, and reporting.

- Back office: Administrative and operational tasks such as settlements, reconciliations, accounting, and documentation.

Banking BPO services across the financial services value chain

The impact of banking BPO and finance services offshoring extends to several business areas and can be seen throughout the lending lifecycle:

- Information technology (IT)

- Finance and accounting (FAO)

- Discrete back office functions

- Contract services

Industry research shows that finance organizations outsource both regulated and unregulated functions within outsourcing contracts that vary in scope and complexity.

Banks and lending institutions typically offshore transactional functions such as new customer acquisition, account servicing, consumer and commercial lending, and back office process management.

Less commonly outsourced are higher-value functions like budgets, forecasts, regulatory returns, and capital management.

Customer acquisition services

Customer acquisition services manage prospective customers and inquiries, bridging marketing and CRM functions. Key capabilities include:

- Lead generation and pipeline management

- Credit evaluation, verification, and approval

- Application intake and onboarding

- Telemarketing, promotions, and referral programs

- Customer support and closed-loop reporting

Account servicing processes

Consumer Accounts

Third parties handle transactional and support functions for consumer accounts, including:

- Customer service (online, phone, email)

- Retail banking and loan originations

- End-to-end consumer lending and mortgage services

- Credit/debit card operations

- Fraud detection, AML, and risk analytics

Commercial accounts

Outsourced commercial account servicing improves cost efficiency and risk management:

- Payment processing: transfers, liquidity, billing, pension/dividends, fraud monitoring

- Commercial loan processing: credit evaluation, underwriting, collateral assessment

- Trade finance: origination, customer support, reconciliation, fraud analytics

Capital markets

BPO services standardize front, middle, and back office processes for capital markets:

- Research, valuations, and model development

- Trade processing, clearing, and settlement

- Data management, analytics, and reconciliations

- Portfolio reporting and compliance support

Consumer and commercial lending services

BPO solutions cover the full lending lifecycle:

- Loan origination, underwriting, approval, and closure

- Mortgage processing and servicing

- Foreclosure, loss mitigation, bankruptcy, and loan modification

- Data management, risk assessment, and portfolio reporting

Back office transaction process management

Back office BPO enables banks to manage complex, non-customer-facing tasks efficiently:

- Fraud detection and risk monitoring

- Anti-money laundering (AML) and KYC support

- Regulatory compliance and reporting

- Custody and asset management services

- Portfolio analytics, accounting, and IT support

Key benefits of business process outsourcing in financial services

By outsourcing business processes, companies can control costs, remain compliant with regulations, and consistently deliver excellent customer service. Banks, fintechs, and other financial institutions can offload non-core processes to expert third-party providers and focus on strategic priorities.

Cost optimization and predictable operating expenses

Outsourcing reduces overhead by eliminating the need for hiring, training, and managing large in-house teams. Organizations gain predictable operating costs and can scale resources up or down based on demand.

Improved compliance and risk management

BPO providers bring domain expertise in regulatory frameworks such as GLBA, PCI DSS, and AML/KYC requirements. They implement standardized controls, automated monitoring, and robust reporting to help mitigate compliance risks and protect sensitive financial data.

Scalability and faster time-to-market

Outsourcing allows banks and lenders to rapidly adjust capacity during peak periods, launch new products, or enter new markets without the delays associated with building internal teams or infrastructure.

Access to specialized BFSI talent

Third-party providers offer access to skilled professionals with deep knowledge of banking, lending, capital markets, and risk management processes. This expertise is often cost-prohibitive to maintain in-house, especially for smaller or mid-sized institutions.

Process standardization and efficiency gains

BPO providers implement streamlined workflows, automation, and best practices across multiple functions, reducing errors, cycle times, and redundancies. Standardized processes improve overall operational efficiency and allow organizations to focus on value-added services.

When should you choose business process outsourcing services?

Here are some of the common scenarios where BPO can deliver the greatest impact:

- Rapid growth or market expansion: Scale operations quickly without hiring and training large internal teams. Supports new products, customer onboarding, and entering new markets efficiently.

- Increasing regulatory burden: Leverage BPO expertise to stay compliant with regulations like GLBA, AML/KYC, and PCI DSS.

- Legacy systems and manual processes: Modernize workflows with automation and digital tools. Reduces errors, speeds up turnaround times, and improves operational efficiency.

- Cost-to-income ratio pressure: Lower operational costs and achieve predictable expenses. Free capital for investment in strategic initiatives while improving profitability

- Need to refocus on core banking activities: Delegate non-core or specialized processes to third parties, allowing internal teams to focus on customer experience, revenue generation, and growth strategies.

Why Sourcefit for banking and financial services outsourcing

Sourcefit is one of the most reliable BPO providers, offering nearshore and offshore solutions to BFSI organizations. We deliver scalable, compliant, and efficient services across the full banking value chain.

From customer support to account services and back office functions, you will be able to free up your budget to invest in revenue-generating processes.

✔️ Flexible staffing models for short- or long-term projects

✔️ Specialized BFSI expertise to ensure accuracy and compliance

✔️ Technology-enabled processes for efficiency, automation, and real-time reporting

✔️ Global support with onshore, nearshore, and offshore options

Conclusion

Business Process Outsourcing is a strategic tool for modern banks and financial institutions. It enables organizations to reduce costs, manage regulatory compliance, scale efficiently, and focus on core banking activities.

By leveraging BPO for both regulated and non-regulated processes across the front, middle, and back office, institutions can stay agile, competitive, and customer-centric.

Sourcefit provides the expertise, technology, and flexible workforce models to help your organization achieve these goals.

Contact us today to explore how BPO can transform your banking operations.

FAQs

Which banking processes are most commonly outsourced?

Transactional functions such as account servicing, loan processing, credit evaluation, back office operations, and customer support are the most frequently outsourced.

Is banking BPO compliant with financial regulations?

Yes, reputable banking BPO providers like Sourcefit adhere to industry standards and regulations like GLBA, AML/KYC, and PCI DSS, ensuring compliance while mitigating risk.

What’s the difference between banking BPO and financial services outsourcing?

Banking BPO is a subset of financial services outsourcing focused specifically on banking functions, while financial services outsourcing can cover broader sectors, including insurance, investment management, and capital markets.